Coin card, one year later

24/Aug 2014

One year after my first (and - so far - only) blog post about Coin, the company seems to be in trouble: backers are (rightfully) concerned about the product launch postponed for six months, and commentators ask what are the future plans for the product after its target market - the US - adopt EMV chip cards.

It seems most of the backers are concerned about the future in regards to the rollout of chip cards in the US, but the FAQ on coin website don’t do much to address the concern, insisting it will work during US’ EMV transition period and if it has a magnetic stripe.

As I highlighted one year ago, I think EMV is not the main issue. Let me clarify.

Coin always claimed it was working with merchants on acceptance, but haven’t received endorsement from major retailers. That’s one part of the problem: as reported by CNN, the Coin card does not look like a normal credit card, and it’s easy to see how merchants outside of the Bay Area tech scene might be skeptical of a credit card that doesn’t look like anything they’ve seen before.

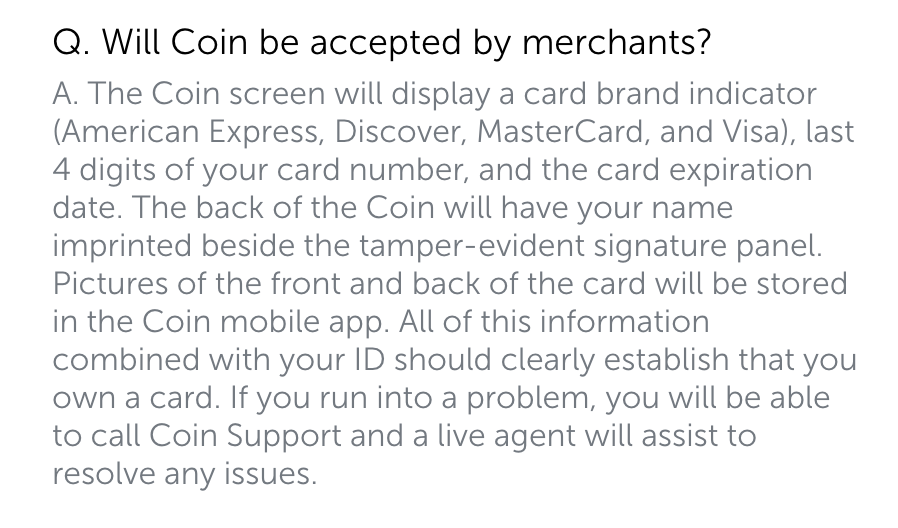

Coin goes on saying, in its FAQ:

Does everyone agrees that those features clearly establish that you own a card? Debatable.

Does everyone agrees that those features clearly establish that you own a card? Debatable.

Moreover, in many jurisdictions, the rule is still “the merchant is not permitted to accept a credit card […] without presentation of the credit card“.

I think Coin should offer the convenience of a “one card to store them all” together with the convenience of not relying on a smartphone to work. Work with issuers and merchants (to guarantee acceptance) and with regulators (to overcome the legal requirement of presenting the card in certain jurisdictions) is paramount for its success.

Failing that, disillusioned customers may be able to use coins for hotel loyalty cards, and not much more. But will be the likes of Hilton willing to accept it? ;)